Investing fundamentals

EditCompound returns, asset allocation, custody, taxes — the literacy required to deploy capital without losing it to fees or confidence-trap mistakes.

What this skill unlocks

Investing literacy is the gate to every capital-deployment idea on TierIncome. Without it, you’ll over-pay for advice, panic-sell at bottoms, leave 1-2% APY on the table to fees, miss tax-advantaged accounts, and confuse yield with safety. The asymmetry between literate and illiterate investors is 2-3× lifetime returns on the same capital.

The economic reality: a 30-year-old who deploys $200/month into index funds for 35 years at 8% real return ends with $430K. The same person paying 1.5% advisor fees ends with $290K. The literacy gap is $140K of free money — that’s the ROI of 40-80 hours of reading.

This skill is knowledge-heavy, not technique-heavy. There’s no “deliberate practice” to get good at it like copywriting or video editing. You read, internalize the principles, deploy small amounts to practice the emotional discipline, then scale capital as you accumulate it.

What “competent” looks like

You’re competent when you can:

- Explain compound returns to someone with a calculator example, including the tax-deferred account difference.

- Pick an asset allocation appropriate to your age, income volatility, and goals. Defend it.

- Choose a brokerage based on fees, custody quality, geographic constraints. Avoid known bad actors.

- Read a fund fact sheet (expense ratio, tracking error, top holdings, allocation drift).

- Resist behavioral traps — recency bias, sunk cost, FOMO, status anxiety. Stick to your plan during 30%+ drawdowns.

- Understand tax efficiency — accounts (401k, IRA, ISA, depending on geo), tax-loss harvesting, asset location.

Steps 1-4 take 30-50 hours of reading. Steps 5-6 take real money in a real account through real volatility — typically 24-60 months.

How to actually practice

The trap: paralysis-by-research. People read 5 books and never invest. The pattern:

- Open a brokerage account NOW (Fidelity for US, Trading 212 / Interactive Brokers for EU). 30 minutes.

- Buy ONE all-world index ETF (VT or VWCE) with whatever you have to deploy. The point is starting the emotional clock, not optimization.

- Read the Bogleheads’ Guide in 3-week stretches. Don’t sprint; let principles sink in.

- Set up automatic monthly contributions — even $50/month. The discipline is the asset, not the amount.

- Don’t check the account daily. Quarterly review at most. Allocate the saved attention to skill-building or income-earning.

- At month 12, expand into specific products if you have a thesis (REITs, dividend stocks, P2P, crypto staking). NOT before. The first year is for emotional baseline.

Where to apply it on TierIncome

- Dividend stock portfolio — investing fundamentals are the entire prerequisite.

- REITs — sector + tax considerations require basic literacy.

- P2P lending (EU) — risk-vs-yield framework comes from this skill.

- Crypto staking + DeFi lending (Aave/Compound) — same risk frameworks; different platforms.

- Buy a website — multiples + cash flow + risk analysis are pure investing thinking.

- Crypto trading bots — even active trading requires position sizing + drawdown psychology from this skill.

Honest realities

- Most active investing underperforms index funds. 80-90% of professional managers underperform the S&P 500 over 10+ years. The chance you (a retail investor with hours/week to commit) beat them is small. Default to index funds; deviate only with explicit thesis.

- Yield is risk-adjusted, not absolute. A 12% APY P2P platform isn’t “better” than a 4% high-yield savings account — it’s compensating you for higher default risk. Compare risk-adjusted, not raw.

- Tax efficiency beats asset selection for most retail investors. Maxing tax-advantaged accounts (401k, IRA, ISA) before optimizing what’s IN them is the highest-leverage move.

- Crypto is a small allocation idea for most. 0-10% of portfolio is reasonable for those with conviction. Beyond that, you’re trading, not investing — different skill.

If you read the Bogleheads’ Guide + open a brokerage + automate monthly contributions for 12 months, you’re already in the top 30% of retail investors by behavior. The compounding from years 5-30 is where the math gets life-changing — and that’s just continuing the boring early habits.

Where to learn it

The resources we'd actually use, sorted by type. Affiliate links are tracked through /go/[slug].

Books (4)

The single best beginner investing book. Boring on purpose. Index funds, asset allocation, tax-deferred accounts, behavioral pitfalls. If you read ONE book on this list, this is it.

Classic that demolishes most active-investing myths. Teaches efficient-market thinking + index-fund discipline. Pair with Bogleheads' Guide for the full passive-investing mental model.

Warren Buffett's stated favorite. Dense, dated, but the foundational text on value investing + market psychology. Read AFTER the Bogleheads book; it's a level deeper.

Modern complement to Bogleheads — same core philosophy with 2026-relevant data + tactics. Specifically practical for young investors with smaller portfolios.

Communitys (2)

The single most rigorous investing community on the internet. Wiki articles on tax-loss harvesting, asset location, lazy portfolios are freely available. Lurk for 4 weeks before posting questions.

r/Bogleheads is rigorous + pro-index-fund. r/personalfinance is broader (debt, taxes, life decisions). Both better than Twitter finance noise. Skip r/wallstreetbets unless you're studying behavioral pitfalls.

Tools (3)

Morningstar Premium

PaidFund + ETF + stock analysis. Skip until you're managing $50K+ — free tier is enough for asset allocation decisions. Pricey for general retail investors.

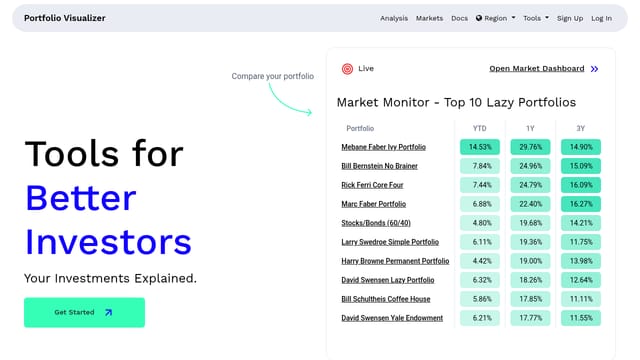

Portfolio Visualizer

FreemiumBacktest portfolio allocations against historical data. The single most-used tool by serious DIY investors. Free tier covers most use cases. Upgrade only at $100K+ AUM.

Custody is the second-most-important investing decision after asset allocation. Fidelity + Vanguard for US (no fees). Interactive Brokers for global. Avoid Robinhood for serious money.

Newsletters (1)

Best free investing newsletter in 2026. Specifically about retail-investor decision-making backed by data. Read his book Just Keep Buying alongside; the writing is dense and practical.